$30M Series A · Lead investor sought

PYROTECH is the molten-salt recycling technology that turns used nuclear fuel back into fuel — safely, on-site, without producing weapons-grade plutonium. Asset-light. Licensing-based. Built for the renaissance that's already here.

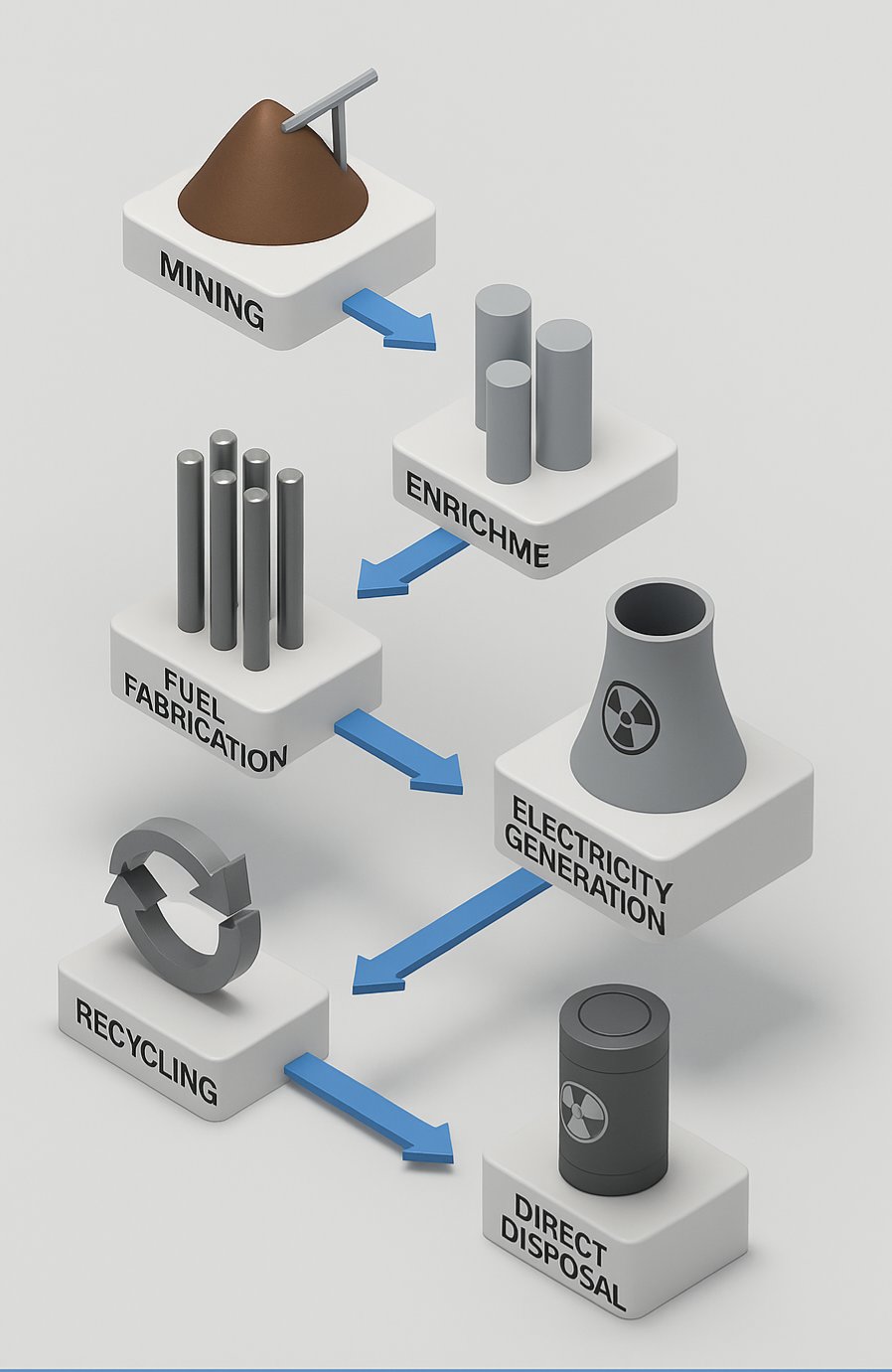

The problem

Every gigawatt of nuclear power makes ~25,000 kg of used fuel a year. The global fleet keeps growing. The two ways the industry has to handle it are both broken — and waste is now the gating factor for the nuclear renaissance.

Deep geological disposal runs $300–2,700/kg, buries material that still has value, and hands governments a permanent liability that's politically radioactive. Community opposition delays and cancels reactors before they're built.

Conventional aqueous reprocessing is expensive and complex, can't handle hot fuel, separates pure plutonium (a proliferation problem), and leaves behind highly radioactive liquid waste. Effectively a state monopoly.

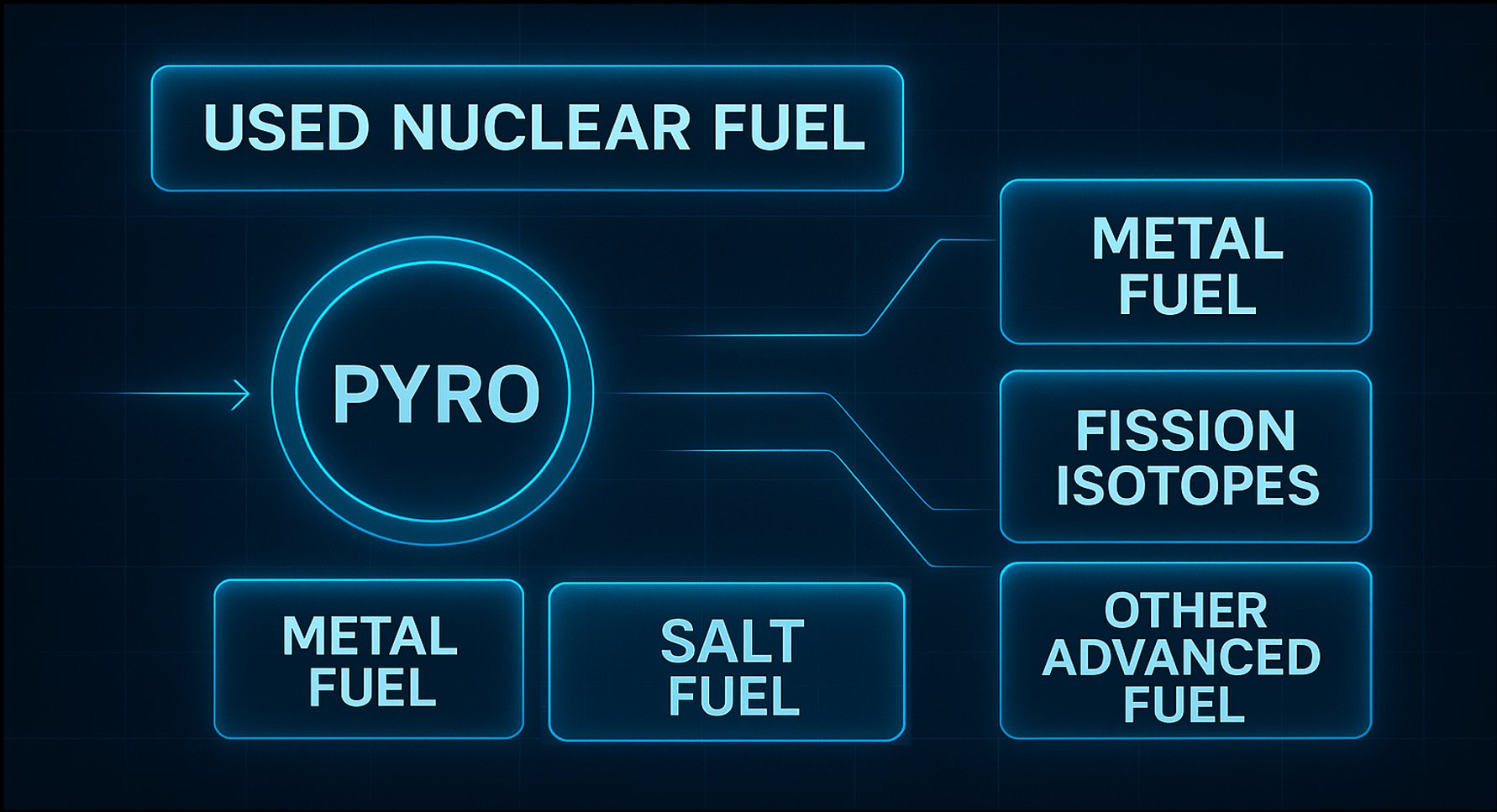

The breakthrough · PYRO

PYRO is a direct chemical reduction process developed in Prof. Jinsuo Zhang's lab at Virginia Tech. It recovers uranium and the actinides as fuel — and crucially, never isolates a pure plutonium stream.

Why now · the renaissance

After decades of stagnation, nuclear is being built again at scale: tripling pledges, restarts, and a wave of new reactors driven by AI-era electricity demand. Capacity is the headline. Used fuel is the part nobody has solved — and it grows in lockstep with every gigawatt added.

Hyperscalers and governments are racing to bring reactors online — new builds, SMRs, and restarts of idled plants. Each added gigawatt is ~25,000 kg more used fuel a year that someone is legally obligated to manage.

The U.S. and allied governments have made domestic nuclear capacity and fuel sovereignty firm policy — backed by executive orders, tripling commitments and waste-fund obligations.

The NRC and international bodies are actively friendly to advanced nuclear innovation. Early pre-licensing engagement now lowers downstream approval risk.

The economics

Against a ~$1,300/kg global average for used-fuel management. Cost target anchored to U.S. DOE / Argonne pilot-scale estimates.

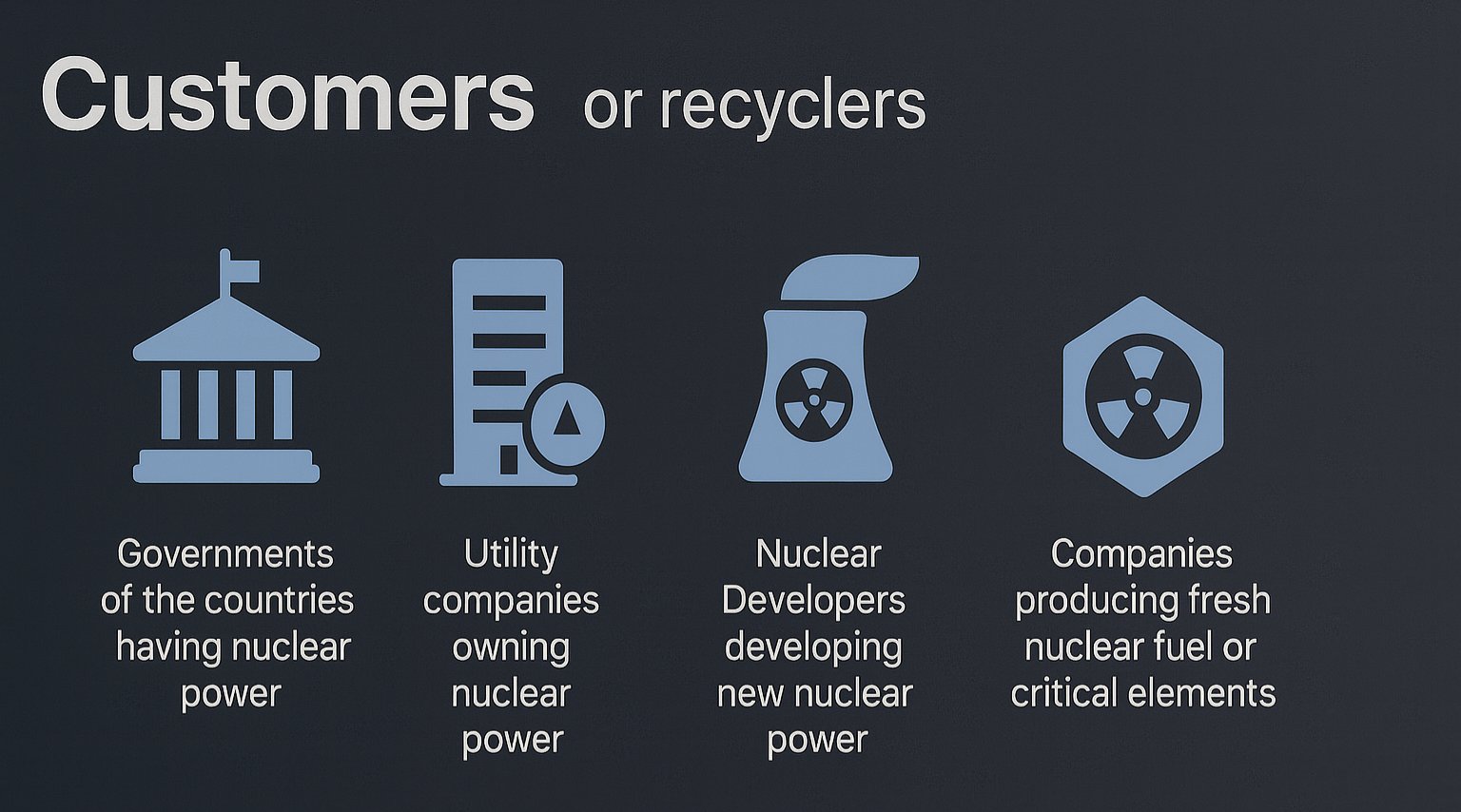

The model

Recyclers, utilities and governments carry the manufacturing and operating risk. PYROTECH owns the IP and earns three stacked, recurring fees — a Tesla-style asset-light spread on a global hardware fleet.

A percentage of projected gross margin, paid when a licensee signs. Cash in early, before a single module is built.

15% of actual gross margin, every year, on every kilogram a licensee recycles. Scales with the installed fleet.

$100k per module per year. A per-unit annuity that compounds as modules multiply across sites and countries.

The landscape

The team

A world authority in pyroprocessing and molten-salt systems. He demonstrated the core PYRO process — complete reduction of UO₂ to metallic uranium, no anode, no external power — and holds the trade secrets and know-how behind it.

Delivered and licensed the only operating molten-salt reactor in the world (China, 2011–2018). Led reactor and fuel-recycling licensing with Canada's CNSC. Architected a 500 MW project in Indonesia. Raised and deployed $400M+ for nuclear programs.

A capital-markets bench built for cross-border energy deals.

The plan

Most of the work is engineering, IP and partnerships, not concrete and steel. That lets PYROTECH compress the path: patents in 90 days, a complete Phase 1 in 24 months, and licensing revenue while peers are still permitting their first site.

Core IP locked and owned by PYROTECH within 90 days of close.

Engineering design finalized, lab validation done, Korea manufacturing plan set, NRC pre-licensing underway, customer & licensee MOUs signed.

A built, tested system validating performance and the economic model (Phase 2).

First licensees sign and pay — the recurring fee engine starts turning.

Standardized modules deploying across plants and countries worldwide.

The technology is ready. The team has licensed first-of-a-kind nuclear before. The market is obligated to buy.

Request the data room